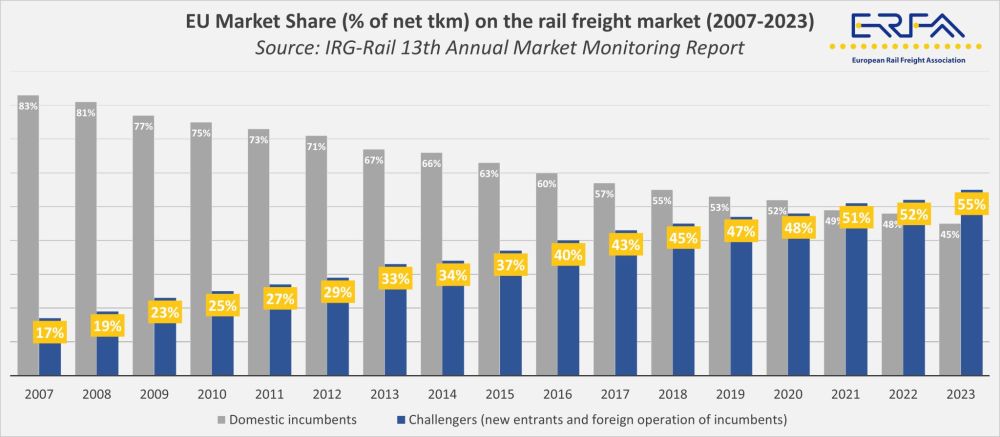

According to the latest Market Monitoring Report by the Independent Regulators Group (IRG-Rail), competitors reached a 55% share of the European rail freight market in 2023.

This shift in market structure has taken place against the background of an overall decline in transported volumes. Infrastructure works, increased road competition, and lower industrial output across Europe contributed to a difficult year for rail freight operations.

The data indicates diverging trajectories for market participants. Larger incumbent operators, including DB Cargo and Hexafret (previously operating as SNCF Fret), are expected to scale down their activities as a result of decisions linked to competition law. The space left behind is gradually being filled by smaller or newer rail freight undertakings entering liberalised markets.

However, the 55% market share figure represents an average across EU Member States. National markets still show wide discrepancies, and the presence of barriers—particularly those limiting international services—remains a structural issue. Domestic conditions and the level of openness to new operators continue to define the competitive landscape in individual countries.

Beyond market share data, the ERFA report draws attention to infrastructure-related challenges. Disruptions from planned works and insufficient capacity management have contributed to service reliability issues, especially on key international corridors. Calls are being made for Member States to ensure long-term and stable funding for infrastructure managers to organise work schedules in a way that provides predictability for operators.

Current policy debates are also shaped by the upcoming Railway Infrastructure Capacity Regulation, revisions to the Technical Specifications for Interoperability (TSIs), and the ongoing rollout of ERTMS. These processes are being monitored closely by the freight sector, with concerns over rising compliance costs and their effect on market access for smaller players.

Additional pressure points include energy pricing and access to electricity markets for traction purposes. Disparities in the way externalities are handled between rail and road transport also continue to affect competitive dynamics.